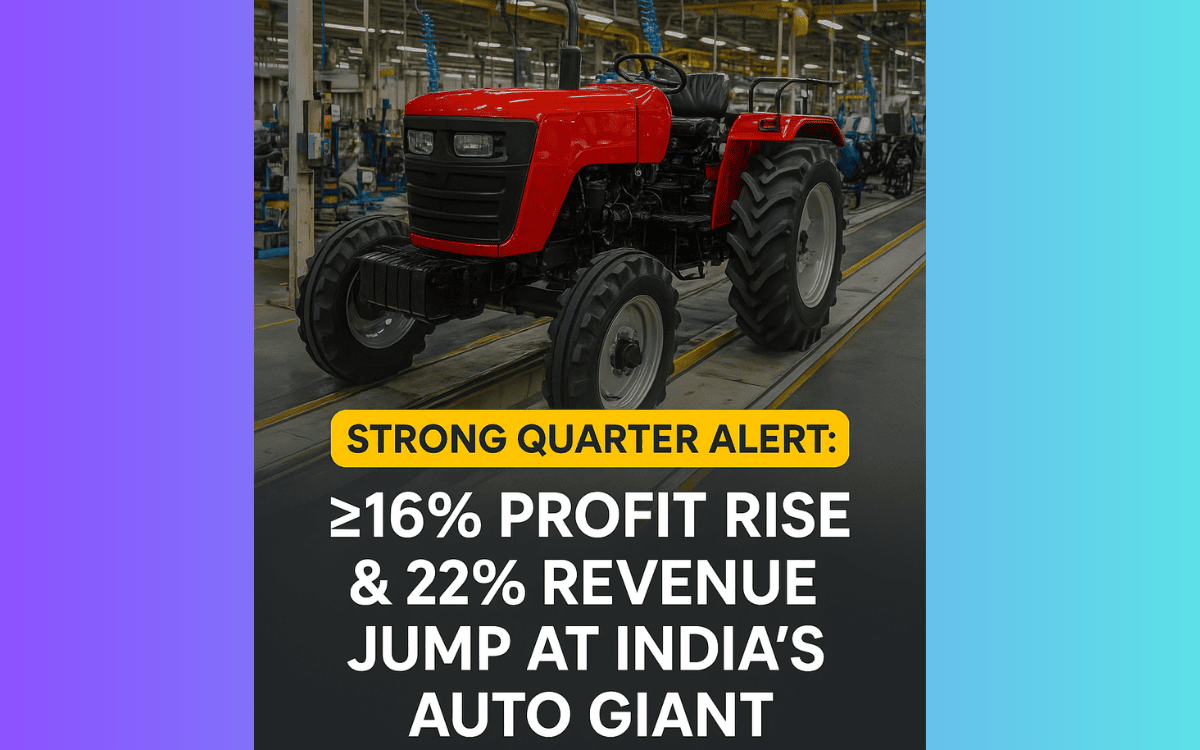

India’s auto sector is showing renewed strength, with one of the major players posting robust second-quarter results that underscore both operational resilience and market demand. The maker of tractors, SUVs and off-road vehicles saw net profit climb more than 16 % year-on-year, while revenue surged approximately 22 % for the quarter under review.

In more detail: The company reported a consolidated profit after tax of about ₹3,673 crore for Q2 FY26, compared to roughly ₹3,160 crore in the same period a year ago. Simultaneously, its total income grew to nearly ₹66,300 crore from around ₹54,500 crore in Q2 FY25 — a growth of 21.7 %.

Several factors are contributing to this strong performance. First, demand in both the auto and farm-equipment segments remains healthy, particularly aided by rural incomes and export growth. Second, the company has managed cost pressures better than many peers, with raw material inflation and supply-chain disruptions showing signs of easing. Third, a favourable product mix—leaning toward higher-margin vehicles and value-added offerings—has helped the bottom line expand.

However, it’s not entirely smooth sailing. While the growth numbers are impressive, the macroeconomic background remains tricky: weak global demand, rising input costs, and currency headwinds could still dampen future momentum. The company itself points to ongoing vigilance around commodity inflation, interest-rate rises and inventory management.

For investors, the key takeaway is this: although the top-line surge is significant, the sustainability of margins and the ability to convert revenue into cash-flow will determine how far the upside can go. Watching how the business manages working capital, export dynamics and product launches will be important in coming quarters.

The auto-maker’s management has also reiterated its strategy of expanding its presence in electric and hybrid vehicles, increasing localisation of inputs and enhancing after-sales service to drive recurring revenues. These structural initiatives may take time to pay off, but they are visible in the Q2 commentary.

In conclusion: This quarter’s results are a clear win, signalling that the company is capturing favourable tailwinds in demand and market share. But the broader environment remains complex. If you’re a reader of Home to Heart, it’s a good moment to assess exposure to companies with strong earnings momentum, healthy balance sheets and credible transformation plans. A 20 %+ revenue jump paired with double-digit profit growth is noteworthy—but keep an eye on forward risks.